Auditors Try to Achieve Independence in Appearance in Order to

The previous chapter emphasized the importance of auditor independence and objectivity to internal auditing and noted the challenge to achieve true independence in internal auditing. Become independent in fact.

Pdf Auditor Independence In Fact Research Regulatory And Practice Implications Drawn From Experimental And Archival Research

Become independent in appearance and in fact C.

. Maintain an unbiased mental attitude. Comply with the generally accepted auditing standards D. If internal audit is to retain its necessary independence in practice it must take the time to invest in its relationships with the board audit committee key business stakeholders and senior management sustaining a steady and robust dialogue with each party in order to perpetuate its own functional success.

A CPA while performing an audit strives to achieve independence in appearance in order to A Reduce risk and liability. Maintain an unbiased mental attitude. Auditors try to achieve independence in appearance in order to A- maintain public confidence in the profession.

Abstract- The American Institute of Certified Financial Accountants is carrying out a reevaluation of the rules concerning audit independenceThe move is intended to tackle the ethical aspects of audit independence in relation to issues such as objectivity integrity and economic interest. Auditors try to achieve independence in appearance in order to ________. Ccomply with the responsibilities principle.

Comply with the responsibilities principle D. The idea that independence is entirely a personal matter which varies from auditor to auditor in a given set of circumstances is not useful in setting standards for all auditors. C Comply with the generally accepted auditing standards of fieldwork.

Maintain an unbiased mental attitude. Amaintain public confidence in the profession. D Maintain an unbiased mental attitude.

B Comply with the generally accepted standards of fieldwork. Auditors try to achieve independence in appearance in order to a Maintain public from COMMERCE 4ad3 at McMaster University. The AICPA Code of Professional Conduct requires that members in public practice be objective free of conflicts of interest and independent in fact and appearance section 300050.

D Maintain public confidence in the profession. C Become independent in fact. B maintain public confidence in the profession.

Maintain an unbiased mental attitude. Independence is considered by many to be of paramount importance to the effectiveness of the audit function and increasingly the public media critics and regulatory agencies have questioned if auditors are sufficiently independent of their clients in fact and appearance. 4 maintain an unbiased mental attitude.

Independence requires integrity and an objective approach to the audit process. Auditor independence meaning independence of both the firm engaged to perform external audits and the individual auditors who conduct the auditsis a central facet of external auditing. Auditors try to achieve independence in appearance in order to.

The ability to be objective does not well serve the auditor or the client if no one believes that the auditor can be objective in a given set of circumstances. Maintain public confidence in the profession B. Auditors try to achieve independence in appearance in order to maintain public confidence in the profession The preparation of an audit plan prior to the beginning of fieldwork is appropriately considered documentation of.

Perception or Reality. A Maintain public confidence in the profession. The concept requires the auditor to carry out his or her work freely and in an objective manner.

Become independent in fact 3. The Conceptual Framework for AICPA Independence Standards defines independence in appearance as. The SEC likewise requires independence by the external auditors who perform an audit of managements assertions in the registrants financial report.

B Become independent in fact. To do that the audit committee must have a complete understanding of the services their auditor has provided and is providing and a general understanding of the independence rules and the concerns that those rules seek to address. Maintain public confidence in the profession O 4.

Maintain public confidence in the profession B. An auditor strives to achieve independence in appearance to. D-maintain an unbiased mental attitude.

Comply with the generally accepted auditing standards of field work. Dmaintain an unbiased mental attitude. An auditor strives to achieve independence in appearance to O 1.

Become independent in fact. Auditors try to achieve independence in appearance in order to. By Jacobson Peter D.

Comply with the auditing standards related to audit performance O 2. Aintain public confidence in the profession come independent in fact mply with the responsibilities principle aintain an unbiased mental attitude QUESTION 13 Auditors try to achieve independence in appearance in orc maintain public confidence in the profession. 3 comply with the generally accepted auditing standards of fieldwork.

Auditor Independence And Objectivity. C-comply with the responsibilities principle. Auditors try to achieve independence in appearance in order to.

1 maintain public confidence in the profession. Become independent in fact C. The avoidance of circumstances that would cause a reasonable and informed third party having knowledge of all relevant information including safeguards applied to reasonably conclude that the integrity objectivity or professional skepticism of a firm or a.

Audit committees must be able to spot independence issues as early as possible in order to avoid impairment. ESTION 13 ors try to achieve independence in appearance in order to. 2 become independent in fact.

Maintain public confidence in the profession. An auditor strives to achieve independence in appearance to 1 maintain public confidence in the profession. Bbecome independent in fact.

Auditor independence refers to the independence of the internal auditor or of the external auditor from parties that may have a financial interest in the business being audited. B-become independent in fact.

Previous Study On Factors Influencing Auditor Independence In Appearance Download Scientific Diagram

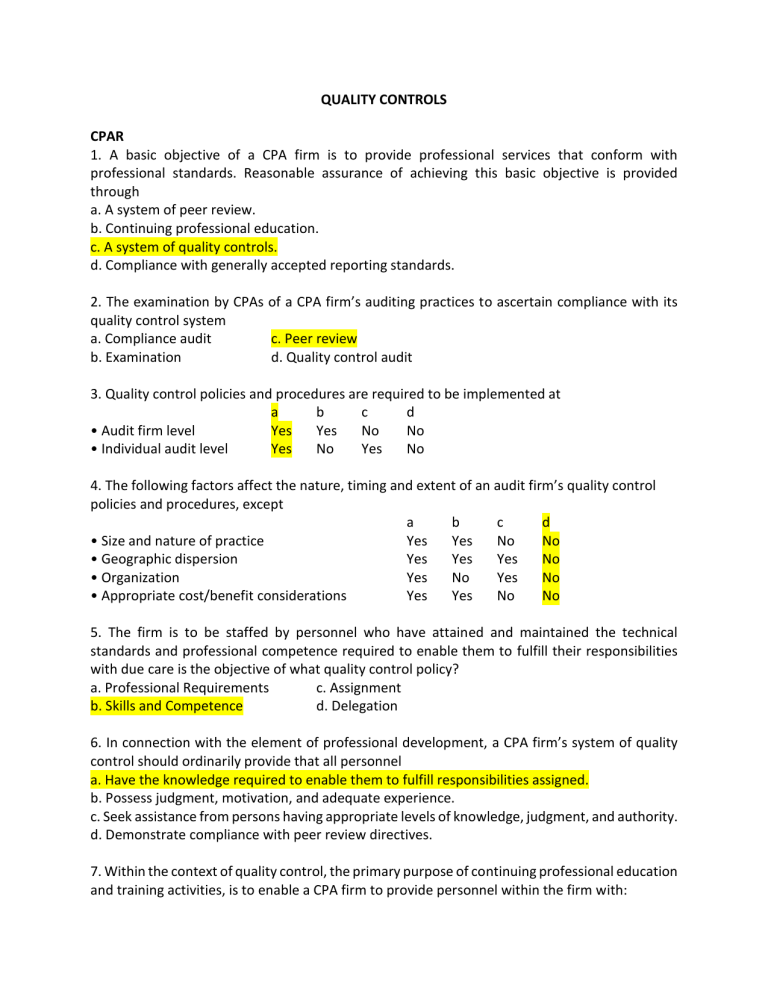

Quality Controls Reviewer

Et Section 101 Independence Pcaob

2

Independensi Dalam Fakta Independen In Fact Ada Bila Auditor Benar Benar Mampu Course Hero

Pdf Audit Quality And Auditors Independence

Now Is The Time To Operationally Split Audit And Nonaudit Services The Cpa Journal

2

Standard On Auditing Sa 200 Revised Overall Caalley Com

Independence In Fact Vs Independence In Appearance Youtube

Lecture Slide Chapter 3 Professional Ethics Independence And Audit

Pdf Is It Time For Auditor Independence Yet

Previous Study On Factors Influencing Auditor Independence In Appearance Download Scientific Diagram

2

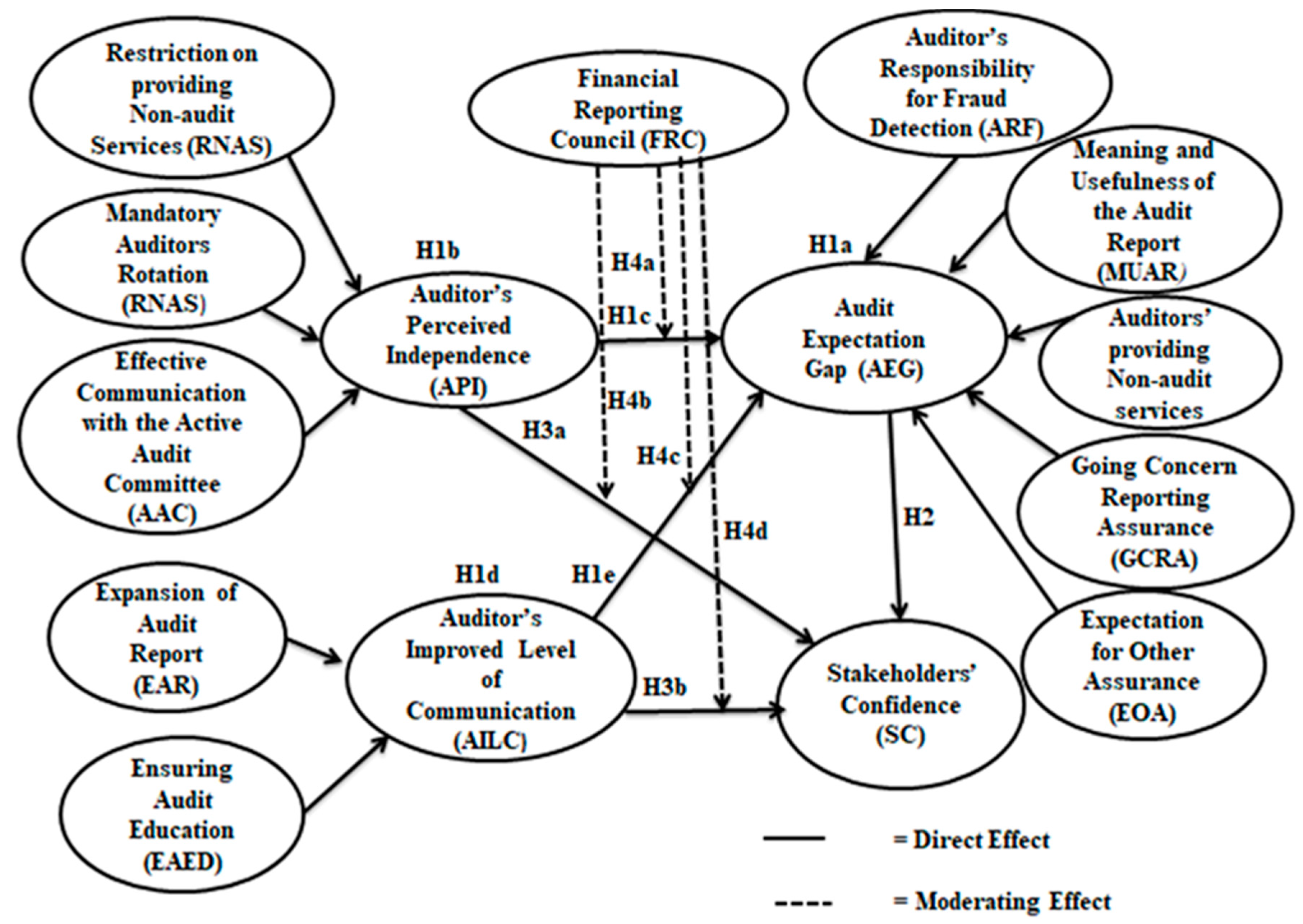

Ijfs Free Full Text Existence Of The Audit Expectation Gap And Its Impact On Stakeholders Confidence The Moderating Role Of The Financial Reporting Council Html

2

2

Distinguish Between Independence In Fact And Independence In Appearance State Course Hero

Research Proposal On Threat To Auditors Independence Accounting Essay History Reveals That Audit Studocu

Comments

Post a Comment